(Japanese: 成本 迅)

Affiliation

Department of Psychiatry (Psychiatric Functional Neuroscience), Graduate School of Medical Science, Kyoto Prefectural University of Medicine (Professor, 2016– )

Overseas / Public Roles

Member, National Dementia Policy Promotion Council (Dementia Basic Act); METI Dementia Innovation Alliance WG; Visiting Senior Researcher, Consumer Affairs Agency

Major Research Fields

Old-Age Psychiatry · Dementia & Decision-Making Support · Financial Gerontology · Psychiatric Neuroimaging (OCD, dementia) · Non-pharmacological & Digital Interventions

Professor Jin Narumoto is a psychiatrist and a nationally recognized authority on dementia care, geriatric psychiatry, and decision-making support for older adults. He pioneered the clinical assessment of medical decision-making capacity in Japan and helped establish the field of financial gerontology, which seeks to protect the financial decision-making and economic rights of people living with dementia. Through his influential books, assessment tools, and policy-oriented research, he has played a leading role in shaping clinical and societal approaches to dementia care. In parallel, he contributes the Kyoto cohort to the international ENIGMA-OCD Consortium, advancing global research on obsessive–compulsive disorder through large-scale neuroimaging and psychiatric data analysis. To date, he has authored 270 scientific publications and 18 books.

Professor Narumoto’s work bridges academic research, clinical practice, and national policy. He serves on the national Dementia Policy Promotion Council established under Japan’s Dementia Basic Act, participates in the Dementia Innovation Alliance Working Group of the Ministry of Economy, Trade and Industry (METI), and is a Visiting Senior Researcher at the Consumer Affairs Agency. His research is supported by a JST RISTEX social-implementation project, for which he serves as principal investigator, focused on supporting healthcare decision-making among older adults with dementia, as well as multiple KAKENHI Grants-in-Aid for Scientific Research.

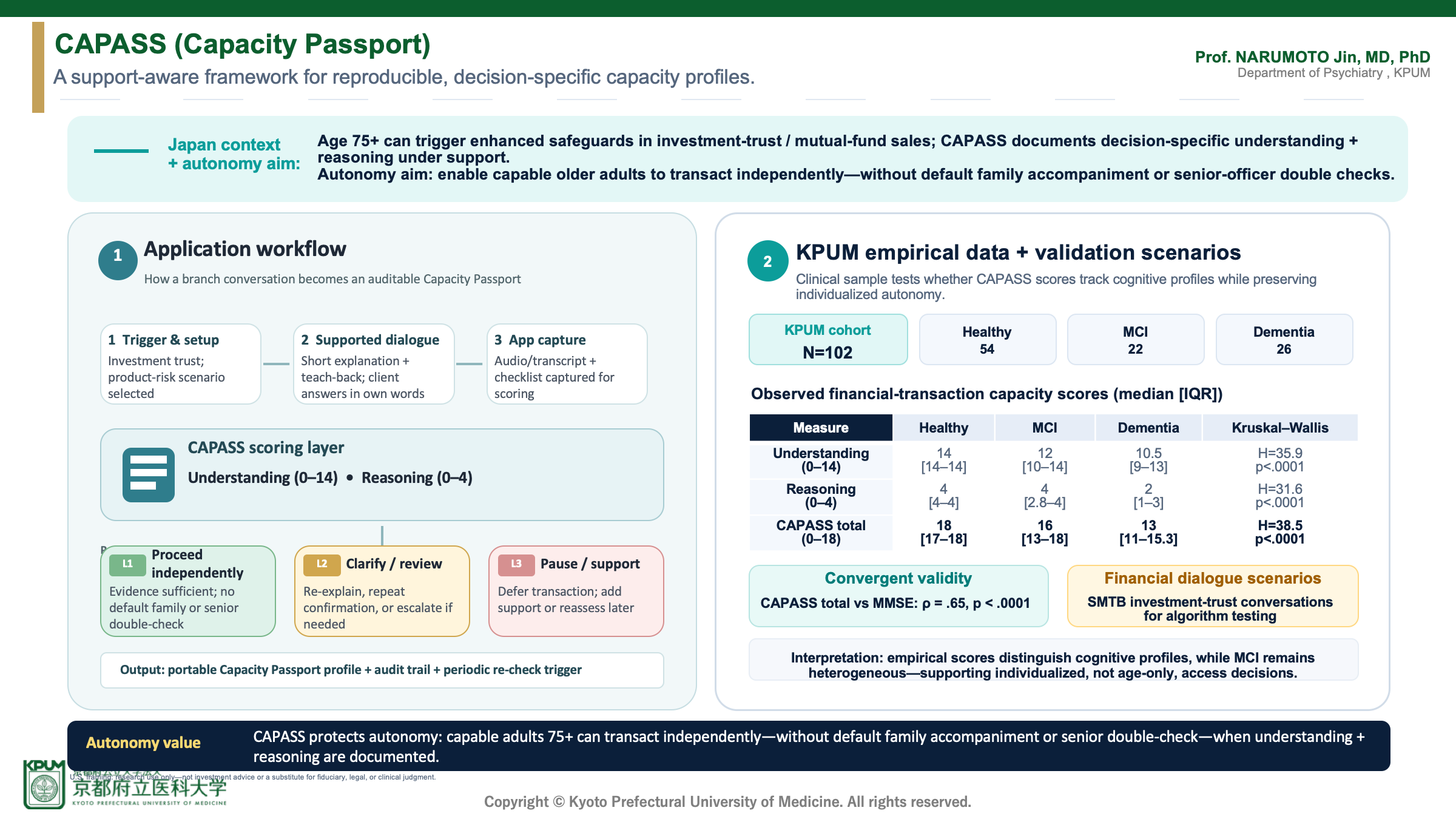

Today I am introducing CAPASS, which stands for Capacity Passport. The Japanese implementation context is important: in investment-trust, or mutual-fund, sales, clients aged 75 and older often face enhanced suitability safeguards and practical transaction procedures.

The key point is that CAPASS is not intended to add another restriction. It is designed as an autonomy-preserving mechanism. The goal is to avoid using chronological age alone as a proxy for incapacity. When CAPASS documents that an older adult has adequate understanding and reasoning for the specific investment-trust transaction, with appropriate support if needed, it can create an auditable basis for allowing that person to trade independently — without default family accompaniment or a senior-officer double check.

The left-hand panel now shows the practical application workflow. First, the transaction is registered in the app: for example, a client aged 75 or older is considering an investment trust, and the staff member selects the relevant product-risk scenario. Second, the staff member conducts a supported conversation, using short explanations and teach-back questions so the client answers in their own words. Third, the app captures the interview as audio or text, together with a structured checklist.

CAPASS then converts that dialogue into an evidence-based profile. The algorithm focuses on two functional domains: understanding and reasoning. Understanding covers whether the client grasps the product, risks, alternatives, costs, and consequences. Reasoning covers whether the client can compare options and explain why the choice fits their goals, financial situation, and tolerance for loss.

Operationally, the result is not just a score; it is a procedure branch. In an L1 case, the evidence is sufficient and the client can proceed independently, without making family accompaniment or a senior-officer double check the default. In an L2 case, the system prompts re-explanation, repeated confirmation, or review. In an L3 case, the transaction is paused and additional support or reassessment is considered. In every branch, CAPASS produces an auditable Capacity Passport profile that can support quality assurance, complaints prevention, and periodic re-checking.

The right-hand panel adds empirical evidence from Kyoto Prefectural University of Medicine, or KPUM. The current dataset includes 102 participants: 54 healthy older adults, 22 older adults with mild cognitive impairment, and 26 patients with dementia. The median age was 81 years across the groups. CAPASS total scores were highest in the healthy group, with a median of 18 out of 18, lower in the MCI group, with a median of 16, and lowest in the dementia group, with a median of 13. The group difference in CAPASS total score was statistically significant, with Kruskal–Wallis H of 38.5 and p less than .0001.

The same pattern appears in the two functional domains. Understanding and reasoning both separated the cognitive groups statistically, while the MCI group still showed substantial retained capacity in many cases. This is important for the CAPASS concept: capacity is heterogeneous, and it should be assessed with decision-specific evidence rather than inferred from age or diagnostic label alone.

The KPUM data also support convergent validity. CAPASS total score correlated with MMSE at rho .65, with Trail Making Test Part B at rho minus .59, and with WMS-R Logical Memory II at rho .64, with all p-values less than .0001. In other words, CAPASS is aligned with established cognitive measures but remains focused on the functional question that matters for a given transaction: can this person understand and reason about this decision under appropriate support?

The autonomy-relevant finding is especially important. Among participants with MMSE scores of 24 to 26, 51 percent achieved high CAPASS total scores of 17 or above out of 18. This means that even within a mild cognitive impairment range, many individuals may retain sufficient transaction-specific understanding and reasoning. For CAPASS, this supports supported assessment and individualized evidence, rather than automatic exclusion based on age or cognitive screening alone.

In parallel, CAPASS is being tested in realistic financial dialogue scenarios through joint research with Sumitomo Mitsui Trust Bank. These scenarios are based on investment trusts sold by the bank and are used to test whether the algorithm can evaluate capacity-related features in actual advisory-style conversations.

The goal is not to replace clinical, legal, or fiduciary judgment. The goal is to make the evidence for autonomy and safeguards more reproducible, auditable, and individualized.

Operating at the intersection of medicine, ethics, and society is our CAPASS initiative. In aging societies, cognitive decline often triggers restrictive financial safeguards. CAPASS shifts the paradigm from age-based restriction to evidence-based autonomy.

It assesses a patient’s specific ability to reason through a decision, producing an auditable cognitive profile. Our data shows that many individuals with mild impairment maintain high decision-making capacity — allowing us to actively protect their independence.

Research Inquiries

For inquiries regarding the research profiles featured on this page,

please contact us at: